Introduction: Why Shared Mobility Is Entering a Global Scale-Up Phase

Shared Mobility’s Shift From Experimentation to Infrastructure Layer

Shared mobility has moved beyond its origins as a convenience-led urban experiment. Early ride-hailing, bike-sharing, and car-sharing pilots were largely confined to dense metropolitan areas and targeted digitally savvy users. Today, shared mobility is increasingly viewed as a core component of urban and peri-urban transport systems rather than an optional alternative.

This shift reflects a broader maturation of the sector. Platform operators are no longer optimizing only for rapid user growth. Instead, they are focused on geographic expansion, service diversification, and integration with public transport, logistics, and energy systems. Shared mobility is becoming embedded in how cities and regions plan movement of people, not just how consumers book a ride.

Why Global Expansion Is Accelerating Now

The current phase of global scale-up is being driven by structural factors rather than cyclical demand. Multiple forces are converging to make shared mobility economically and politically relevant across both developed and emerging markets.

Key drivers shaping this acceleration include:

- Rapid urban population growth increasing pressure on existing transport infrastructure

- Rising cost of private vehicle ownership in major cities

- Government mandates focused on congestion reduction and emissions control

- Widespread smartphone penetration and digital payment adoption

- Improved operational efficiency through data, automation, and AI-driven routing

Together, these factors are expanding the addressable market for shared mobility far beyond early adopter cities and into tier-two cities, suburban corridors, and developing economies.

From Local City Plays to Multi-Region Platforms

One of the most important changes in the shared mobility landscape is the transition from city-specific operations to multi-country and multi-region platforms. Leading companies are building standardized technology stacks that can be localized for regulatory, cultural, and infrastructure differences.

This shift has important business implications. Expansion strategies now emphasize:

- Regulatory partnerships with city and national governments

- Asset-light or hybrid ownership models to manage capital intensity

- Local fleet partnerships and franchise-style rollouts

- Cross-selling of services such as ride-hailing, micromobility, and subscriptions

As a result, shared mobility platforms increasingly resemble global infrastructure businesses rather than local transport startups.

Why Shared Mobility Matters Beyond Transportation

Shared mobility is no longer just a transport category. It sits at the intersection of several high-impact economic and policy priorities, which elevates its strategic importance for a wide range of stakeholders.

Its relevance extends into:

- Energy transition through electric vehicle deployment and charging ecosystems

- Smart city initiatives using mobility data for urban planning

- Labor markets through flexible, platform-based work models

- Automotive industry transformation away from private ownership

- Digital ecosystems combining payments, mapping, and data services

Because of this convergence, shared mobility decisions increasingly influence investment flows, regulatory frameworks, and long-term urban development strategies.

Shared Mobility Explained: Definition, Models, and Ecosystem Overview

What Shared Mobility Means in Today’s Transportation Economy

Shared mobility refers to transportation services that provide users with short-term, on-demand access to vehicles or rides without ownership. These services are typically digital-first, app-enabled, and usage-based, allowing users to pay per trip, per minute, or through subscriptions rather than bearing the fixed costs of owning a vehicle.

From a systems perspective, shared mobility is designed to increase asset utilization across vehicles, roads, and energy infrastructure. By reducing idle time and improving demand matching, shared mobility introduces economic efficiency into urban and regional transport networks. This efficiency logic is what enables shared mobility to scale across income groups, geographies, and use cases.

Crucially, shared mobility is not a single market. It is a collection of service models, ownership structures, and ecosystem participants that interact differently depending on local regulation, infrastructure readiness, and consumer behavior.

Core Shared Mobility Service Models

Shared mobility consists of several service models, each optimized for different trip types, distances, and user needs. While these models originated independently, platform convergence is increasingly common as operators seek higher engagement and better unit economics.

Major Shared Mobility Service Models

| Service Model | Primary Use Case | Typical Trip Length | Capital Intensity | Common Markets |

|---|---|---|---|---|

| Ride-hailing / Ride-sharing | Point-to-point passenger transport | Medium to long | Low to medium | Global, urban and suburban |

| Car sharing | Short-term vehicle access | Medium | Medium to high | Urban, airport, corporate |

| Micromobility | First-mile and last-mile trips | Short | Medium | Dense urban centers |

| Peer-to-peer car sharing | Monetizing idle private vehicles | Medium | Low | North America, Europe |

| Mobility subscriptions | Multi-modal access | Variable | Medium | Mature urban markets |

As platforms expand, these models are increasingly bundled within a single app to increase user retention and reduce customer acquisition costs.

Ownership and Asset Structures Behind Shared Mobility

The economic profile of shared mobility businesses is heavily influenced by how vehicles are owned, financed, and operated. Asset structure determines scalability, balance-sheet risk, and the ability to transition fleets toward electrification.

Shared Mobility Asset Ownership Models

| Ownership Structure | Who Owns the Vehicles | Scalability | Capital Risk | Strategic Trade-Off |

|---|---|---|---|---|

| Platform-owned fleet | Operator | Moderate | High | Greater control, higher costs |

| Driver-owned vehicles | Individual drivers | High | Low | Limited control over assets |

| Partner-owned fleets | Fleet operators | High | Medium | Dependency on partners |

| Hybrid ownership | Mixed | High | Medium | Balance of control and scale |

| Public-private fleets | Municipal or state entities | Low to moderate | Low | Regulatory complexity |

Many leading platforms are moving toward hybrid models to maintain operational flexibility while improving service quality and sustainability outcomes.

The Shared Mobility Ecosystem and Value Chain

Shared mobility platforms operate within a multi-layered ecosystem that extends beyond transport services alone. Competitive advantage increasingly depends on ecosystem coordination rather than standalone execution.

Key participants across the value chain include:

- Platform operators managing demand, pricing, and routing algorithms

- Vehicle manufacturers and fleet suppliers providing hardware

- Energy and charging providers supporting electrified operations

- Mapping, navigation, and data service providers

- Governments and regulators shaping operating conditions

Because no single player controls the entire value chain, partnerships and long-term contracts play a critical role in enabling geographic expansion.

How Shared Mobility Differs From Traditional Transport Models

Shared mobility introduces a structurally different approach to transport delivery when compared with both private vehicle ownership and fixed-route public transit systems.

Key differentiators include:

- On-demand access rather than fixed schedules

- Dynamic pricing and routing based on real-time demand

- Faster deployment without heavy infrastructure investment

- Data-driven optimization across fleets and cities

These attributes make shared mobility particularly effective in fast-growing urban regions where transport demand evolves faster than traditional planning cycles.

Why Clear Definitions Matter for Market and Strategy Decisions

Inconsistent definitions of shared mobility often lead to fragmented market estimates and misaligned policy decisions. Some analyses include only ride-hailing, while others bundle micromobility, car sharing, and subscriptions, resulting in wide variance in reported market size.

Establishing a clear framework that distinguishes service models, asset ownership, and ecosystem roles provides a more reliable foundation for market sizing, competitive analysis, and long-term investment planning. As shared mobility matures into a permanent layer of global transport infrastructure, definitional clarity becomes a strategic necessity rather than an academic exercise.

From Local Experiments to Global Platforms: How Shared Mobility Scaled

Early City-Level Pilots and Proof of Concept

Shared mobility initially emerged through tightly scoped city-level pilots. Early ride-hailing, bike-sharing, and car-sharing services were designed to test consumer willingness to shift away from private vehicle ownership in dense urban environments. These pilots focused on solving immediate urban pain points such as congestion, parking scarcity, and last-mile connectivity.

At this stage, scale was not the primary objective. Operators prioritized speed to market, user acquisition, and regulatory survival. Business models were often subsidized, fleets were limited, and unit economics were secondary to validating demand and behavior change.

The Transition From Pilot Projects to Repeatable Playbooks

As adoption stabilized, leading operators began converting localized learnings into standardized operating playbooks. This marked a shift from experimentation to systemization, enabling faster rollout across multiple cities and countries.

This transition was enabled by:

- Modular technology stacks that could be deployed across geographies

- Standardized driver onboarding and fleet management processes

- Replicable regulatory engagement frameworks

- Data-driven demand forecasting and pricing models

Once these elements were in place, expansion costs per city declined, improving scalability and investor confidence.

Platformization and the Rise of Multi-Modal Offerings

Shared mobility’s scaling phase coincided with the rise of platform-based business models. Rather than operating single-mode services, leading players expanded into multi-modal ecosystems combining ride-hailing, micromobility, car sharing, and logistics.

This platformization delivered strategic advantages:

- Higher user engagement through multiple use cases

- Cross-subsidization between high- and low-margin services

- Improved data density for routing and demand prediction

- Reduced customer acquisition costs across services

As a result, shared mobility apps increasingly function as mobility operating systems rather than standalone transport tools.

Geographic Expansion Beyond Tier-One Cities

After establishing dominance in major metropolitan areas, shared mobility platforms shifted focus toward tier-two cities, suburban corridors, and emerging markets. These regions often presented different demand patterns, regulatory environments, and infrastructure constraints.

Key expansion adaptations included:

- Lower-cost vehicle options and pricing models

- Flexible service coverage tailored to lower density areas

- Partnerships with local fleet operators and municipalities

- Integration with informal or semi-formal transport networks

This geographic diversification expanded the total addressable market while reducing overdependence on saturated urban cores.

Capital, Consolidation, and Market Rationalization

Scaling shared mobility globally required substantial capital investment, particularly for technology, incentives, and fleet expansion. Over time, this led to market consolidation as smaller players struggled to achieve sustainable unit economics.

Key Phases in Shared Mobility Scaling

| Phase | Primary Objective | Capital Intensity | Competitive Outcome |

|---|---|---|---|

| Pilot and launch | Prove demand | Low to medium | High fragmentation |

| Rapid expansion | Capture market share | High | Aggressive competition |

| Platform build-out | Improve engagement | Medium | Ecosystem leaders emerge |

| Consolidation | Improve profitability | Medium | Fewer, stronger players |

This rationalization phase has reduced price wars in many markets and shifted focus toward operational efficiency and profitability.

Market Size and Growth Snapshot of the Global Shared Mobility Market

A Market That Has Moved From Niche to Material Scale

The global shared mobility market has transitioned from a niche urban service into a material segment of the broader transportation and mobility economy. Over the past decade, growth has been driven less by novelty and more by structural demand for flexible, cost-efficient mobility solutions across cities and regions.

What is notable about the current phase is not just the size of the market, but its breadth. Shared mobility now spans passenger transport, micromobility, corporate mobility, and adjacent services such as delivery and logistics. This expansion has widened the addressable market well beyond early ride-hailing use cases.

Rather than growing evenly, the market has expanded in waves, shaped by regional regulation, infrastructure readiness, and consumer behavior.

Historical Growth Pattern and Market Evolution

Shared mobility growth has followed a distinct multi-stage trajectory. Early growth was rapid but uneven, driven by aggressive expansion in a limited number of large cities. More recently, growth has become steadier and more geographically diversified.

Key phases in market evolution include:

- Initial surge driven by ride-hailing adoption in major metropolitan areas

- Acceleration through micromobility and car-sharing additions

- Temporary slowdowns linked to regulatory pushback and pandemic disruptions

- Recovery and expansion supported by diversification, electrification, and enterprise use cases

This pattern has resulted in a market that is larger, more resilient, and less dependent on a single service model or geography than in its early years.

Market Size Composition by Service Type

The shared mobility market is best understood as a portfolio of service segments with different growth dynamics, margins, and capital requirements. Ride-hailing remains the largest contributor, but faster growth is increasingly coming from complementary segments.

Shared Mobility Market Composition by Segment

| Segment | Relative Market Share | Growth Momentum | Strategic Importance |

|---|---|---|---|

| Ride-hailing and ride-sharing | Largest | Moderate | Revenue backbone |

| Micromobility | Medium | High | Urban density and sustainability |

| Car sharing | Smaller | Moderate | Corporate and premium use cases |

| Peer-to-peer sharing | Smaller | Moderate | Asset-light expansion |

| Subscriptions and bundles | Emerging | High | Customer retention and ARPU growth |

This mix explains why leading platforms prioritize ecosystem expansion rather than relying on a single mode for growth.

Regional Contribution to Global Market Growth

Market size and growth rates vary significantly by region, reflecting differences in urbanization, income levels, vehicle ownership, and regulatory frameworks.

Broad regional patterns include:

- North America contributing significant revenue but slower incremental growth

- Europe showing steady expansion supported by sustainability policies

- Asia-Pacific driving the largest share of new user growth

- Emerging markets contributing volume growth with lower revenue per user

As a result, global market growth increasingly depends on a balance between high-revenue mature markets and high-growth emerging regions.

Why Market Size Alone Is an Incomplete Metric

While market size provides useful context, it is not sufficient for strategic decision-making. Differences in margin structure, capital intensity, and regulatory risk mean that equal revenue does not translate into equal value across segments or geographies.

For operators and investors, understanding where growth is profitable, defensible, and scalable is more important than headline market numbers. This perspective sets the stage for deeper analysis of regional dynamics, demand drivers, and competitive positioning in the sections that follow.

Key Shared Mobility Segments: Ride-Hailing, Car Sharing, and Micromobility

Shared mobility is often discussed as a single market, but its underlying segments differ significantly in economics, user behavior, and scalability. Ride-hailing, car sharing, and micromobility each serve distinct mobility needs and respond differently to regulation, urban density, and infrastructure quality.

Understanding these segments individually is essential for assessing where growth is sustainable, where margins are under pressure, and how platforms prioritize investment across their service portfolios.

Global Usage Distribution of Shared Mobility

The above distribution represents an estimated global usage split of shared mobility services, synthesized from public company disclosures, regional adoption trends, and industry mobility analyses. Ride-hailing continues to dominate due to its global scale and deep penetration across North America, Asia-Pacific, and Latin America. Micromobility maintains strong momentum in dense urban centers driven by sustainability mandates and short-distance travel demand. Car sharing remains structurally smaller but stable, particularly in Europe and metropolitan markets with high vehicle ownership costs. These figures should be interpreted as directional market estimates rather than audited global statistics.

Ride-Hailing and Ride-Sharing: The Revenue Anchor

Ride-hailing remains the largest and most visible shared mobility segment globally. It addresses medium- to long-distance, point-to-point travel and benefits from strong network effects once scale is achieved.

This segment is characterized by:

- High trip frequency in dense urban and suburban areas

- Asset-light or hybrid ownership models using driver-owned vehicles

- Dynamic pricing driven by real-time demand and supply

- Heavy regulatory scrutiny related to labor and pricing

Ride-hailing’s strategic value lies in its revenue scale and data generation, even as profitability remains uneven across regions.

Car Sharing: Flexibility Between Ownership and Access

Car sharing occupies a middle ground between private vehicle ownership and ride-hailing. Users gain temporary access to vehicles for longer, self-driven trips without long-term ownership commitments.

Car sharing typically appeals to:

- Urban residents with occasional driving needs

- Corporate and institutional users

- Airport and intercity travel segments

Car Sharing Model Variants

| Model Type | Vehicle Ownership | Typical Use Case | Capital Intensity | Common Markets |

|---|---|---|---|---|

| Station-based | Operator-owned | Planned trips | High | Europe, Asia |

| Free-floating | Operator-owned | Spontaneous urban trips | High | Dense cities |

| Peer-to-peer | Private owners | Cost-sensitive users | Low | North America, Europe |

While capital-intensive, car sharing offers higher control over service quality and is often easier to electrify than ride-hailing fleets.

Micromobility: Solving the Short-Distance Problem

Micromobility services, including shared bikes, e-bikes, and e-scooters, are designed for short-distance and first-mile or last-mile travel. Their rise reflects changing urban travel patterns and the push for low-emission transport options.

Key characteristics of micromobility include:

- Short trip durations and high daily usage potential

- High dependence on urban density and infrastructure

- Strong alignment with sustainability and climate goals

- Sensitivity to city-level regulation and parking rules

Micromobility often delivers lower revenue per trip but plays a critical role in user acquisition and modal integration within broader mobility platforms.

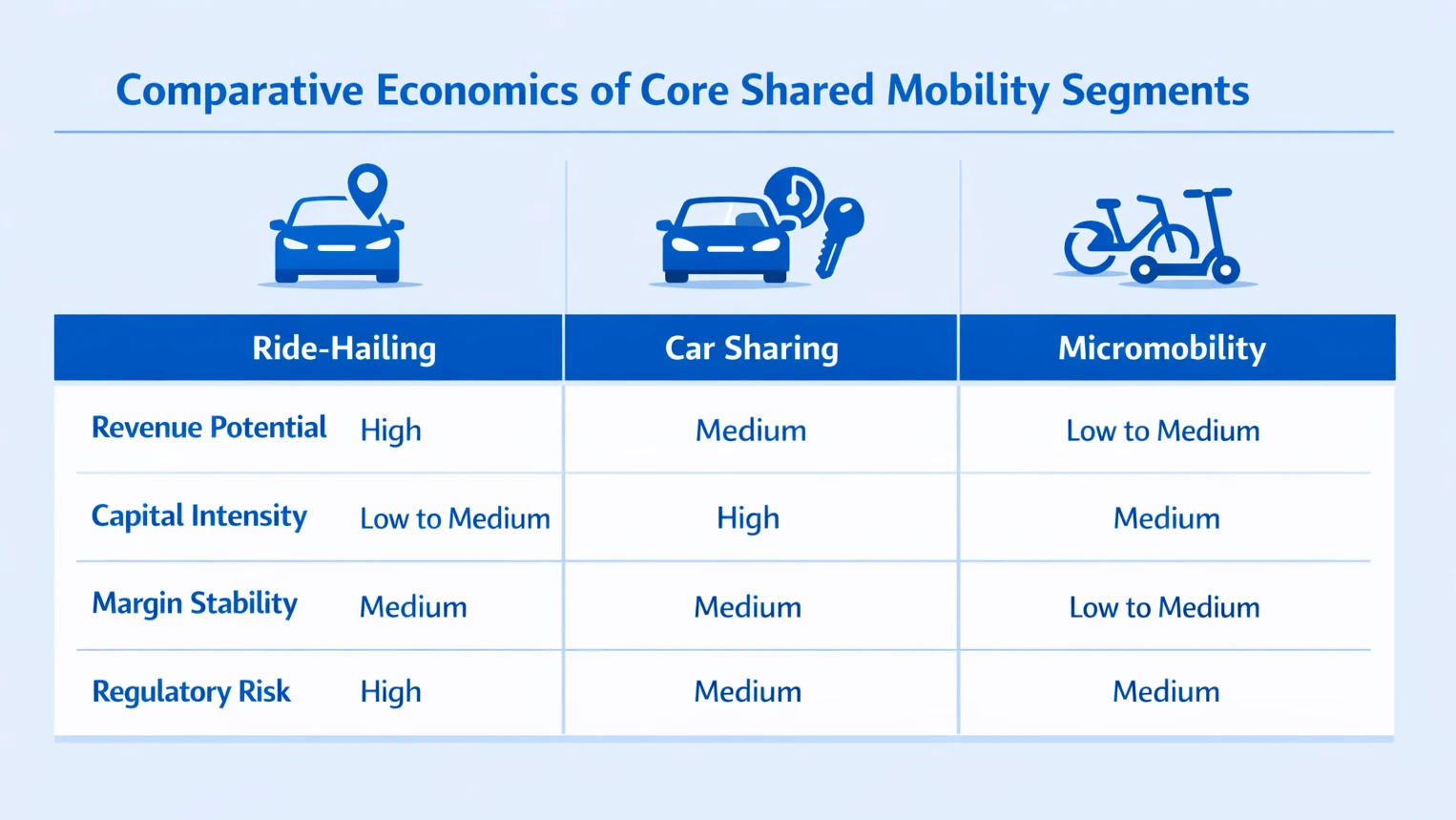

Comparative Economics Across Core Segments

Each shared mobility segment exhibits a distinct economic profile shaped by fleet costs, utilization rates, and regulatory exposure.

Comparative Economics of Core Shared Mobility Segments

The image highlights clear economic differences across shared mobility segments. Ride-hailing offers the highest revenue potential with relatively low to medium capital intensity, but faces significant regulatory risk, particularly around labor and pricing rules. Car sharing requires higher upfront capital due to fleet ownership, resulting in more stable but moderate margins and medium regulatory exposure. Micromobility operates with lower revenue per trip and moderate capital needs, with margin stability closely tied to hardware durability and city-level regulatory constraints.

How Platforms Combine Segments for Scale and Retention

Rather than treating segments in isolation, shared mobility leaders increasingly integrate ride-hailing, car sharing, and micromobility into unified platforms. This multi-segment strategy supports higher engagement and more resilient economics.

Strategic benefits of segment integration include:

- Serving multiple trip types within a single app

- Increasing user lifetime value through cross-usage

- Smoothing demand fluctuations across time and geography

- Strengthening relationships with cities and regulators

Segment diversity is now a core competitive advantage, positioning platforms to adapt as urban mobility needs continue to evolve.

Regional Expansion Patterns Across North America, Europe, and Asia-Pacific

Why Shared Mobility Expands Differently by Region

Shared mobility does not scale uniformly across the world. Regional differences in urban form, income levels, public transport quality, regulation, and cultural attitudes toward vehicle ownership create distinct expansion paths. As a result, business models that succeed in one region often require material adaptation elsewhere.

For operators, regional strategy has become as important as product strategy. Market leaders increasingly design region-specific playbooks rather than pursuing one-size-fits-all expansion.

North America: Revenue-Heavy but Growth-Constrained

North America represents one of the most mature shared mobility markets globally. Ride-hailing penetration is high in major cities, and consumer awareness is well established. However, incremental growth has slowed as markets approach saturation.

Key regional characteristics include:

- High revenue per trip driven by income levels

- Strong reliance on ride-hailing compared to micromobility

- Regulatory pressure related to labor classification and pricing

- Slower adoption in suburban and low-density areas

In this region, expansion is less about new cities and more about improving margins, diversifying services, and expanding enterprise and subscription offerings.

Europe: Policy-Driven and Sustainability-Focused Growth

Europe’s shared mobility expansion is shaped heavily by public policy. Cities across the region actively promote alternatives to private car ownership through congestion pricing, low-emission zones, and restrictions on vehicle access.

Defining features of the European market include:

- Strong micromobility and car-sharing adoption

- High integration with public transport systems

- Municipal control over fleet sizes and operating permits

- Faster electrification of shared mobility fleets

European growth tends to be steadier rather than explosive, with operators prioritizing regulatory alignment and long-term city partnerships over rapid scale.

Asia-Pacific: Volume-Led Expansion at Massive Scale

Asia-Pacific is the largest growth engine for shared mobility by user volume. Rapid urbanization, lower private vehicle ownership rates, and high population density create favorable conditions for shared transport services.

Regional dynamics typically include:

- High trip volumes with lower revenue per ride

- Strong presence of two-wheelers and micro-vehicles

- Super-app ecosystems combining mobility, payments, and delivery

- Government involvement in platform oversight and pricing

Expansion in Asia-Pacific often prioritizes scale, coverage, and affordability, with profitability achieved through ecosystem bundling rather than per-trip margins.

Comparative Regional Dynamics

While all three regions support shared mobility growth, they do so through fundamentally different mechanisms.

Regional Expansion Characteristics

| Region | Primary Growth Driver | Revenue Profile | Regulatory Environment | Strategic Focus |

|---|---|---|---|---|

| North America | Monetization | High per trip | Litigation-heavy | Margin optimization |

| Europe | Policy alignment | Medium | City-led | Sustainability integration |

| Asia-Pacific | Urban density | Low per trip | State-influenced | Scale and ecosystem play |

This divergence explains why global platforms increasingly decentralize decision-making and empower regional leadership teams.

Implications for Global Expansion Strategy

Regional variation means that success in shared mobility depends on adaptability rather than replication. Operators that treat regional differences as strategic inputs rather than operational constraints are better positioned to scale sustainably.

Key strategic implications include:

- Designing pricing and fleet strategies locally

- Aligning early with regulators rather than reacting post-launch

- Accepting different profitability timelines by region

- Leveraging partnerships to accelerate market entry

Understanding these regional expansion patterns sets the foundation for analyzing emerging markets, which represent the next frontier of shared mobility growth.

What Is Driving Global Shared Mobility Adoption

The Structural Forces Powering Market Expansion

Shared mobility growth is no longer fueled by novelty or venture capital subsidies. It is increasingly underpinned by structural economic, technological, and regulatory forces that are reshaping how cities move people and goods. These drivers operate across both developed and emerging markets, though their intensity varies by region.

At a macro level, shared mobility sits at the intersection of urbanization, digitization, and sustainability. As these forces accelerate, shared mobility shifts from being an alternative transport option to becoming a necessary mobility layer.

Urban Congestion and Infrastructure Constraints

Rapid urban growth has outpaced traditional transport infrastructure in many regions. Building metro systems and highways requires significant capital and long timelines, while shared mobility platforms can scale far more quickly.

Key pressure points include:

- Rising traffic congestion in major metropolitan areas

- Limited parking availability in dense city centers

- High capital costs for expanding public transit networks

- Growing commuter demand in peri-urban zones

Shared mobility provides a flexible and faster-deployable solution that can complement public systems without requiring large infrastructure investments.

Rising Cost of Private Vehicle Ownership

In many urban markets, owning a private vehicle is becoming less economically attractive. Fuel prices, insurance premiums, parking fees, congestion charges, and maintenance costs continue to rise.

This shift is particularly evident in:

- Large metropolitan areas with congestion pricing

- Younger demographics delaying car purchases

- Households prioritizing subscription-based consumption models

As total cost of ownership increases, access-based mobility models become more financially rational for certain trip types.

Digital Infrastructure and Platform Maturity

The widespread penetration of smartphones, mobile payments, and real-time navigation technologies has fundamentally enabled shared mobility to scale. Without robust digital infrastructure, demand-supply matching at scale would not be viable.

Critical enablers include:

- High smartphone adoption across income segments

- Seamless digital payment ecosystems

- GPS-based routing and optimization systems

- Cloud computing supporting real-time operations

As digital infrastructure deepens globally, the barriers to entry for shared mobility expansion decline, particularly in emerging markets.

Electrification and Sustainability Mandates

Environmental regulation is becoming a direct catalyst for shared mobility adoption. Many cities are introducing low-emission zones, electrification targets, and vehicle restrictions that incentivize fleet-based solutions over private cars.

Shared mobility aligns well with sustainability objectives because:

- Fleet electrification can be implemented faster than individual vehicle turnover

- Higher utilization improves environmental efficiency per vehicle

- Data-driven routing reduces unnecessary mileage

- Micromobility supports zero-emission short trips

In policy-driven markets, sustainability mandates are accelerating adoption beyond purely economic motivations.

Enterprise and Institutional Adoption

Corporate travel, employee mobility programs, and institutional transport contracts are emerging as stable demand sources for shared mobility platforms. This enterprise segment offers more predictable revenue compared to purely consumer-driven demand.

Growth factors include:

- Companies reducing company car fleets

- Shift toward flexible and hybrid work arrangements

- Corporate sustainability reporting requirements

- Integration of mobility services into employee benefit programs

Enterprise adoption strengthens revenue stability and reduces exposure to purely consumer demand volatility.

Technology Enablers Powering the Shared Mobility Economy

Digital Infrastructure as the Backbone of Scale

Shared mobility would not exist at global scale without advances in digital infrastructure. What began as simple ride-matching apps has evolved into complex, data-driven platforms capable of coordinating millions of daily transactions in real time.

Technology is no longer a support function in shared mobility. It is the core differentiator. Platforms compete on routing efficiency, demand forecasting accuracy, pricing optimization, and system uptime. As markets mature, technology sophistication increasingly determines margin performance.

Core Technology Layers Behind Shared Mobility Platforms

Shared mobility platforms operate on multi-layered technology stacks that integrate user interfaces, real-time logistics systems, and data analytics engines.

Key technology layers include:

- Mobile applications enabling booking, payments, and trip tracking

- GPS and mapping systems for real-time routing and navigation

- Cloud infrastructure supporting scalable operations

- AI-driven demand prediction and dynamic pricing engines

- Payment gateways and digital wallet integrations

These layers work together to reduce friction, increase asset utilization, and improve user experience.

Artificial Intelligence and Data Optimization

AI and machine learning have become central to shared mobility performance. The ability to predict demand patterns, optimize driver allocation, and adjust pricing in real time directly impacts profitability.

Applications of AI in shared mobility include:

- Surge pricing optimization based on supply-demand imbalances

- Predictive maintenance for fleet-based vehicles

- Route optimization to reduce idle time and fuel consumption

- Fraud detection and safety monitoring

- Customer churn prediction and retention targeting

As data density increases, leading platforms gain competitive advantages through better algorithms and operational efficiency.

Interoperability and Mobility-as-a-Service Platforms

The next phase of technology development in shared mobility involves interoperability. Rather than operating in isolation, platforms are integrating with public transport systems, ticketing services, and multimodal journey planners.

Emerging technology priorities include:

- Open APIs for public transport integration

- Unified ticketing and payment platforms

- Real-time multimodal trip planning

- Data sharing frameworks with municipalities

These capabilities move shared mobility closer to a broader Mobility-as-a-Service ecosystem, where users can seamlessly transition between transport modes within a single digital interface.

Comparative View: Technology Impact Across Segments

Different shared mobility segments leverage technology in distinct ways, influencing operational complexity and scalability.

| Technology Lever | Ride-Hailing | Car Sharing | Micromobility |

|---|---|---|---|

| Real-time matching | Critical | Moderate | Moderate |

| Fleet management systems | Medium | High | High |

| Dynamic pricing | High | Low | Low |

| Battery monitoring | Low | Medium | High |

| AI route optimization | High | Medium | Medium |

This variation explains why technology investment priorities differ across segments, even within the same platform.

Technology Is Becoming a Competitive Moat

As markets mature and price competition stabilizes, technology becomes the primary source of differentiation. Platforms that can lower cost per trip, increase utilization rates, and improve safety through analytics will outperform those relying solely on geographic expansion.

For founders, operators, and investors, the key takeaway is clear: shared mobility is evolving from a growth-at-all-costs sector into a technology-intensive operational business. Sustainable competitive advantage will increasingly depend on data scale, AI capability, and ecosystem integration rather than first-mover advantage alone.

Role of Electric Vehicles and Sustainability Mandates in Shared Mobility

Electrification Is Reshaping the Economics of Shared Mobility

Electric vehicles are no longer peripheral to shared mobility. They are becoming central to long-term operating strategy. Fleet-based business models are structurally better positioned to accelerate EV adoption compared to private vehicle ownership because utilization rates are higher and replacement cycles are shorter.

For shared mobility operators, electrification is not only about sustainability branding. It directly impacts cost structure, regulatory compliance, and long-term competitiveness.

Higher utilization means:

- Faster recovery of upfront EV purchase costs

- Greater fuel cost savings compared to internal combustion vehicles

- Improved fleet standardization and maintenance predictability

- Stronger alignment with city-level environmental targets

As battery costs decline and charging infrastructure expands, EV integration becomes increasingly economically viable.

Sustainability Mandates as a Growth Catalyst

Across major urban regions, environmental regulation is actively reshaping transport markets. Low-emission zones, congestion pricing, and zero-emission vehicle mandates are accelerating the shift toward shared and electrified mobility.

Policy mechanisms influencing shared mobility include:

- Zero-emission fleet requirements for ride-hailing platforms

- Restrictions on internal combustion vehicles in city centers

- Subsidies or tax incentives for electric fleet adoption

- Public procurement contracts tied to sustainability metrics

These mandates effectively create structural advantages for operators that invest early in electrified fleets.

Comparative Impact of Electrification Across Segments

Electrification affects each shared mobility segment differently depending on asset ownership and usage patterns.

| Segment | Electrification Feasibility | Primary Benefit | Operational Challenge |

|---|---|---|---|

| Ride-hailing | High | Fuel cost savings | Driver adoption and charging access |

| Car sharing | Very high | Fleet standardization | Charging infrastructure density |

| Micromobility | Already electric | Zero tailpipe emissions | Battery lifecycle management |

Micromobility is inherently electric, while ride-hailing and car sharing represent the largest electrification opportunity in terms of emissions impact.

The Broader Sustainability Narrative

Beyond electrification, sustainability expectations extend to data transparency, labor practices, and urban integration. However, EV adoption remains the most visible and measurable indicator of commitment to decarbonization.

As climate policies intensify globally, shared mobility platforms that position themselves as sustainability infrastructure partners rather than purely transport apps will be better positioned to secure regulatory support and long-term growth.

Regulatory Environment and Policy Impact on Shared Mobility Expansion

Regulation Has Become a Structural Operating Factor

Shared mobility has shifted from regulatory confrontation to structured oversight. Most major markets now operate under defined frameworks that shape fleet size, labor rules, pricing transparency, data reporting, and environmental compliance. Regulation no longer determines whether platforms can operate, but how profitably they can scale.

Global Vehicle Composition in Shared Mobility

The above distribution represents an estimated global vehicle composition of shared mobility fleets in 2025, synthesized from public company disclosures, EV adoption data, and micromobility fleet reports. Electric scooters remain dominant due to rapid urban micromobility expansion, particularly in Europe and Asia. Gasoline vehicles still represent a significant portion of ride-hailing fleets in emerging markets, although electric vehicle penetration continues to rise. Electric cars now account for a growing share of shared mobility fleets, driven by sustainability mandates and fleet electrification targets. These figures should be interpreted as directional estimates rather than audited global fleet statistics.

Core Regulatory Levers

Common policy tools influencing platform economics include:

- Driver classification and labor laws

- Fleet caps and licensing requirements

- Fare transparency or pricing controls

- Mandatory data sharing

- Electrification and emissions mandates

These measures directly affect cost structure, expansion speed, and margin potential.

Labor and Fleet Controls as Economic Drivers

Driver classification remains one of the most financially significant issues. Reclassification toward employee status can increase wage, benefit, and compliance costs.

Fleet caps and licensing restrictions also limit rapid scaling, particularly in dense urban markets. While restrictive, these frameworks can reduce competitive volatility once stabilized.

Regional Divergence

Regulatory intensity varies by region:

- North America often evolves through litigation

- Europe emphasizes city-led sustainability alignment

- Asia-Pacific blends national direction with local enforcement

- Emerging markets may operate under evolving frameworks

This divergence requires localized compliance strategies.

Strategic Implication

Regulation now acts as a competitive filter. Platforms with strong compliance systems, policy engagement, and capital flexibility are better positioned to scale sustainably.

In the mature phase of shared mobility, regulatory alignment is not a constraint to manage. It is a core strategic capability.

Consumer Behavior Shifts Reshaping Shared Mobility Demand

Access Over Ownership Is Becoming Mainstream

A major driver of shared mobility growth is the shift from vehicle ownership to on-demand access. Urban consumers, particularly younger demographics, increasingly prioritize flexibility, cost transparency, and digital convenience over long-term ownership commitments.

This shift is reinforced by:

- Rising total cost of car ownership

- Urban living with limited parking

- Comfort with app-based services and subscriptions

Shared mobility is increasingly viewed as a long-term solution rather than a temporary alternative.

Multimodal and Price-Sensitive Behavior

Consumers are combining ride-hailing, micromobility, and public transit depending on price, distance, and urgency. Demand is highly responsive to pricing, especially in price-sensitive markets.

Key behavioral patterns include:

- Switching modes during surge pricing

- Using micromobility for short trips

- Responding strongly to promotions and loyalty incentives

Platforms that balance pricing transparency with dynamic optimization retain users more effectively.

Trust, Safety, and Sustainability Matter

Adoption is closely tied to perceived safety and reliability. In-app tracking, driver verification, and transparent pricing strengthen trust.

Additionally, environmental awareness is influencing mobility choices, particularly in policy-driven regions. Users increasingly favor electric ride options and low-emission transport modes.

Behavioral Drivers Across Regions

Consumer motivations differ across mature and emerging markets.

| Region Type | Primary Adoption Driver | Secondary Driver |

|---|---|---|

| Mature markets | Convenience and flexibility | Sustainability |

| Emerging markets | Affordability and access | Income opportunity for drivers |

| High-density Asia | Speed and congestion avoidance | Ecosystem integration |

| Europe | Environmental alignment | Public transport integration |

Recognizing these behavioral nuances allows platforms to tailor messaging, pricing, and service offerings by region.

Consumer behavior shifts toward flexibility, digital engagement, and sustainability are structural rather than temporary. Platforms that align pricing, safety, and electrification strategies with these evolving preferences will sustain long-term demand across diverse markets.

Enterprise and Corporate Use Cases for Shared Mobility Platforms

Enterprise Demand Is Becoming a Stable Growth Pillar

Shared mobility is expanding beyond individual consumers into enterprise and institutional segments. Corporations are increasingly integrating ride-hailing, car sharing, and micromobility into employee travel and commute programs.

Enterprise adoption offers:

- More predictable revenue streams

- Higher contract value per client

- Lower acquisition cost compared to retail users

This shift reduces reliance on purely consumer-driven demand.

Corporate Travel and Fleet Alternatives

Many companies are replacing company-owned fleets and taxi contracts with shared mobility partnerships.

Common enterprise use cases include:

- Business travel within cities

- Employee commute programs

- Airport and intercity transfers

- Centralized billing and expense integration

This model supports hybrid work patterns and reduces capital expenditure on owned vehicles.

Revenue Stability and Margin Implications

Enterprise and institutional contracts tend to offer more predictable demand compared to individual consumer usage. However, they often involve negotiated pricing and service-level agreements.

Consumer vs Enterprise Shared Mobility Demand

| Dimension | Consumer Segment | Enterprise Segment |

|---|---|---|

| Demand predictability | Variable | High |

| Pricing flexibility | Dynamic | Contract-based |

| Customer acquisition cost | High | Lower per contract |

| Revenue per account | Low to medium | High |

| Retention potential | Moderate | High |

While enterprise margins may be lower per trip, customer lifetime value is typically higher.

Enterprise mobility is evolving from a supplementary revenue stream to a core growth pillar. Platforms that combine operational reliability, sustainability alignment, and corporate integration capabilities will strengthen revenue stability and long-term scalability.

Top Shared Mobility Companies: Competitive Intelligence Overview

The shared mobility industry is shaped by a mix of global multi-modal platforms, regional champions, and specialized operators across ride-hailing, car sharing, and micromobility. Below is a structured competitive overview including positioning, recent developments, and financial context where publicly available.

Revenue of Major Shared Mobility Players

The chart highlights the significant revenue concentration within the global shared mobility industry. DiDi Global (Est. ~$28.5B) and Uber’s Mobility segment (Est. $25.1B) clearly dominate the sector, reflecting their large-scale ride-hailing operations across China, North America, and other international markets. Lyft, operating primarily in North America, generated $6.3B, positioning it as a strong regional player but at a substantially smaller scale than the two global leaders. Grab’s Mobility segment ($1.2B) reflects its diversified super-app strategy, where mobility represents just one part of a broader ecosystem including delivery and fintech. Smaller platforms such as BlaBlaCar and Getaround (Est.) operate at niche scale, underscoring the steep scale differential and high capital intensity required to compete at global mobility platform levels.

Ride-Hailing & Multi-Modal Platforms

Uber Technologies Inc.

Headquarters: San Francisco, United States

Founded: 2009

Core Segments: Ride-hailing, food delivery, freight, micromobility (limited), enterprise mobility

Competitive Positioning

- Global footprint across North America, Europe, Latin America, Middle East, and parts of Asia-Pacific

- Multi-modal ecosystem combining mobility and delivery

- Strong enterprise mobility integration

Recent Strategic Developments

- Increased focus on profitability and cost discipline

- Expansion of Uber for Business corporate programs

- Continued electrification commitments across major markets

Financial Snapshot

- Publicly listed on NYSE

- Achieved sustained profitability milestones post-pandemic

- Revenue diversified between mobility and delivery segments

DiDi Global Inc.

Headquarters: Beijing, China

Founded: 2012

Core Segments: Ride-hailing, two-wheeler mobility, limited international presence

Competitive Positioning

- Dominant domestic Chinese platform

- Deep integration with local regulatory frameworks

- High trip volume scale

Recent Strategic Developments

- Restructuring after regulatory scrutiny in China

- Refocused primarily on domestic market operations

- Gradual stabilization of operations post-delisting from U.S. markets

Financial Snapshot

- Privately traded after U.S. delisting

- Revenue primarily driven by domestic mobility services

Grab Holdings Limited

Headquarters: Singapore

Founded: 2012

Core Segments: Ride-hailing, food delivery, fintech

Competitive Positioning

- Super-app ecosystem in Southeast Asia

- Strong integration of mobility with payments and financial services

- High user engagement across multiple services

Recent Strategic Developments

- Focus on margin improvement and fintech expansion

- Cost rationalization initiatives

- Strategic partnerships across Southeast Asia

Financial Snapshot

- Publicly listed via SPAC

- Revenue diversified across mobility, delivery, and financial services

Ola Cabs

Headquarters: Bengaluru, India

Founded: 2010

Core Segments: Ride-hailing, EV ecosystem integration

Competitive Positioning

- Strong domestic presence in India

- Expanding EV ecosystem through affiliated ventures

- Competes in highly price-sensitive markets

Recent Strategic Developments

- Expansion of electric vehicle initiatives

- Operational restructuring to improve financial discipline

Car Sharing Platforms

Zipcar

Headquarters: Boston, United States

Founded: 2000

Model: Station-based car sharing

Competitive Positioning

- Strong presence in university and dense urban markets

- Backed by automotive ownership structure

Strategic Focus

- Urban fleet optimization

- Subscription-based usage

Turo

Headquarters: San Francisco, United States

Founded: 2010

Model: Peer-to-peer car sharing marketplace

Competitive Positioning

- Asset-light platform model

- Monetizes privately owned idle vehicles

- Strong presence in North America

Strategic Differentiator

- Marketplace scalability without fleet ownership

Free2move

Headquarters: Paris, France

Parent: Stellantis

Competitive Positioning

- OEM-backed mobility platform

- Integration with manufacturer vehicle pipeline

- Electrification advantage via parent company

Micromobility Operators

Lime

Headquarters: San Francisco, United States

Founded: 2017

Core Offering: E-scooters and e-bikes

Competitive Positioning

- One of the largest global micromobility operators

- Strong regulatory partnerships in Europe and North America

- Focused on profitability after industry consolidation

Tier Mobility

Headquarters: Berlin, Germany

Founded: 2018

Competitive Positioning

- Europe-focused operator

- Emphasis on sustainability and fleet durability

- Strong municipal collaboration model

Bird

Headquarters: United States

Founded: 2017

Competitive Positioning

- Early category pioneer

- Underwent restructuring amid industry consolidation

- Focused on operational optimization

Competitive Landscape Summary

| Category | Market Structure | Competitive Dynamic |

|---|---|---|

| Ride-Hailing | Concentrated, regional dominance | Scale and regulatory depth matter most |

| Car Sharing | Fragmented, OEM influence | Capital intensity shapes competition |

| Micromobility | Consolidating | Policy alignment critical |

Strategic Industry Observations

- The industry has shifted from expansion-at-any-cost to profitability discipline

- Regulatory alignment increasingly acts as a competitive filter

- Electrification readiness is becoming a structural advantage

- Enterprise mobility is emerging as a stabilizing revenue pillar

- Regional champions remain resilient despite global platform ambitions

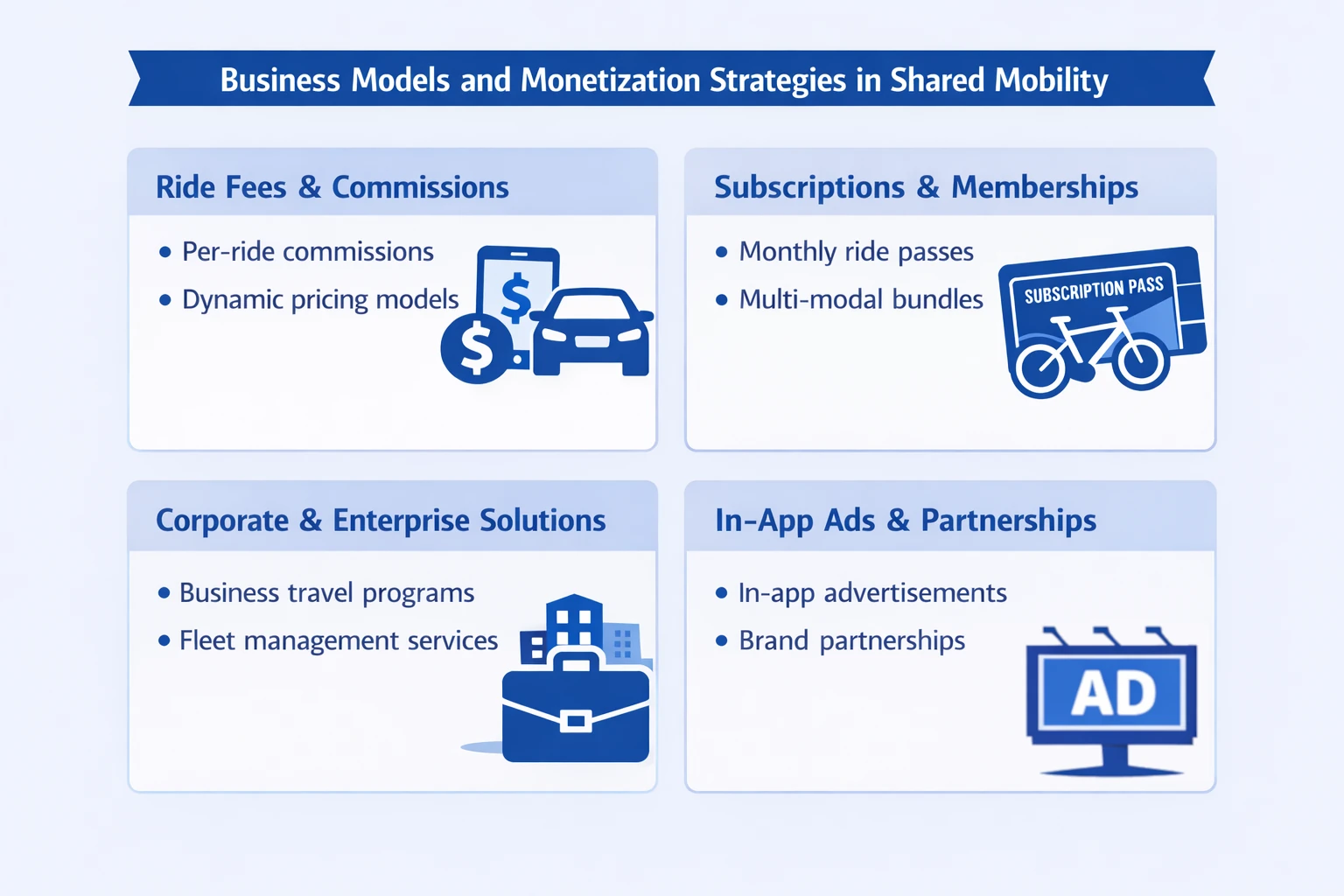

Business Models and Monetization Strategies in Shared Mobility

From Subsidized Growth to Sustainable Monetization

Shared mobility platforms have undergone a significant business model evolution. The early phase of the industry was characterized by aggressive expansion, heavy subsidies, and user acquisition incentives. Today, capital markets and investors demand operational discipline, margin visibility, and diversified revenue streams.

The strategic shift is clear: growth must now be paired with profitability. This has pushed operators to refine monetization models, optimize cost structures, and reduce reliance on incentive-driven demand.

Core Revenue Streams Across Shared Mobility Platforms

Although models differ by segment, most shared mobility companies monetize through a combination of transaction-based and recurring revenue streams.

Primary monetization levers include:

- Commission on ride fares or trip bookings

- Per-minute or per-hour vehicle rental fees

- Subscription or membership programs

- Surge pricing during peak demand

- Enterprise contracts and centralized billing

While transaction commissions remain the backbone, recurring and contract-based revenue is becoming increasingly important for stability.

Comparative Business Models by Segment

Each shared mobility segment operates under distinct economic constraints and revenue logic.

| Segment | Primary Revenue Model | Cost Structure | Margin Drivers |

|---|---|---|---|

| Ride-hailing | Commission-based marketplace | Incentives, platform tech | Utilization rate and pricing efficiency |

| Car sharing | Rental fees | Fleet ownership and maintenance | Fleet utilization and depreciation control |

| Micromobility | Per-minute usage | Fleet hardware and charging | Device durability and lifecycle cost |

Ride-hailing tends to be asset-light but sensitive to driver incentives. Car sharing and micromobility require greater capital deployment but offer stronger operational control.

Subscription and Membership Models

To reduce churn and smooth revenue volatility, platforms are increasingly introducing subscription-based offerings. These programs provide discounted rides, priority access, or bundled services for a fixed monthly fee.

Strategic benefits of subscriptions include:

- Higher user retention

- Predictable recurring revenue

- Reduced price sensitivity

- Increased cross-service usage

Subscriptions are particularly effective in mature urban markets with high usage frequency.

Dynamic Pricing and Yield Optimization

Dynamic pricing remains one of the most powerful monetization tools in shared mobility. By adjusting fares in real time based on demand-supply imbalances, platforms can maximize revenue while managing service availability.

Pricing optimization strategies include:

- Surge pricing during peak periods

- Incentive calibration to balance driver supply

- Time-of-day and location-based adjustments

- Loyalty discounts for high-value users

However, excessive pricing volatility can trigger regulatory scrutiny and damage brand trust, making transparency essential.

Enterprise and B2B Monetization

Enterprise mobility contracts offer higher average revenue per account and lower acquisition costs compared to individual users. Corporate billing, centralized reporting, and emissions tracking create additional value-added services.

Enterprise monetization typically involves:

- Negotiated commission structures

- Subscription or retainer models

- Volume-based pricing agreements

- Integration with expense management systems

This segment enhances revenue predictability and strengthens long-term relationships.

Advertising and Data Monetization

As platforms accumulate high volumes of trip and behavioral data, alternative monetization channels are emerging.

Emerging revenue streams include:

- In-app advertising

- Sponsored ride placements

- Data insights for urban planning

- Partnerships with retail and event venues

While still secondary to core mobility revenue, these channels diversify income and leverage platform scale.

Cost Structure Discipline and Unit Economics

Improving unit economics is central to modern shared mobility strategy.

Key cost components vary by segment but commonly include:

- Driver incentives and subsidies

- Fleet acquisition and depreciation

- Maintenance and charging infrastructure

- Insurance and regulatory compliance

- Technology development and cloud costs

Platforms increasingly focus on reducing cost per trip while increasing average revenue per user.

Strategic Insight: Monetization Is Moving Toward Ecosystem Value

The most successful shared mobility platforms are transitioning from single-service transaction models to ecosystem-based monetization strategies. By combining ride-hailing, micromobility, subscriptions, fintech, and enterprise services, they create multiple revenue touchpoints per user.

The long-term competitive advantage will likely belong to platforms that:

- Balance asset-light scalability with operational control

- Diversify revenue beyond commissions

- Integrate sustainability-linked incentives

- Achieve disciplined capital allocation

As shared mobility matures, monetization sophistication, not geographic expansion alone, will define sustainable market leadership.

Investment Trends, Funding Activity, and M&A in Shared Mobility

From Hyper-Funding to Capital Discipline

Shared mobility has experienced one of the most dramatic capital cycles in modern technology sectors. The early expansion phase was characterized by aggressive venture capital deployment, rapid geographic scaling, and valuation growth driven by network-effect narratives.

Today, the funding environment is markedly different. Investors have shifted focus from gross booking growth to sustainable profitability, positive cash flow, and disciplined capital allocation. This transition has reshaped funding flows, acquisition activity, and exit pathways.

Venture Capital and Early-Stage Expansion

During the sector’s high-growth years, venture capital fueled rapid international expansion, fleet deployment, and user incentives. Ride-hailing and micromobility companies raised multi-billion-dollar rounds to capture market share quickly.

Early-stage capital was typically used for:

- Geographic expansion into new cities

- Subsidizing rider and driver incentives

- Building scalable technology infrastructure

- Acquiring smaller regional competitors

The strategic objective was market dominance rather than near-term profitability.

Public Market Listings and Investor Repricing

Several major shared mobility platforms transitioned to public markets, exposing their business models to greater scrutiny. Public investors placed stronger emphasis on:

- Path to profitability

- Contribution margin improvement

- Operating leverage

- Regulatory risk exposure

This repricing environment reduced tolerance for sustained losses and incentivized cost optimization.

Consolidation and Strategic M&A

As capital tightened and competition intensified, consolidation became a defining feature of the shared mobility landscape. Particularly in micromobility, early overexpansion resulted in mergers, exits, and restructurings.

Drivers of consolidation include:

- Fleet overcapacity in dense urban markets

- Regulatory restrictions limiting device counts

- Difficulty achieving durable profitability at small scale

- Investor pressure for efficiency

Mergers and acquisitions have allowed platforms to strengthen regional positions, reduce competitive intensity, and improve fleet utilization.

OEM and Strategic Investor Participation

Automotive manufacturers and energy companies have increasingly invested in or partnered with shared mobility platforms. These partnerships serve strategic goals beyond financial return.

Strategic motivations include:

- Access to real-world fleet usage data

- Accelerating electric vehicle deployment

- Diversifying revenue beyond vehicle sales

- Participating in mobility-as-a-service ecosystems

OEM-backed mobility brands also reflect a defensive strategy against declining private vehicle ownership in urban areas.

Regional Differences in Investment Patterns

Investment intensity varies across regions:

- North America has seen tighter capital conditions and investor scrutiny

- Europe emphasizes sustainability-aligned funding, especially for electrified fleets

- Asia-Pacific continues to support large-scale ecosystem platforms

- Emerging markets attract strategic capital aligned with long-term growth potential

These regional differences influence platform strategy and expansion timelines.

Private Equity and Late-Stage Restructuring

Private equity participation has increased in later-stage restructuring scenarios. Distressed micromobility firms and underperforming regional platforms have become acquisition targets for investors seeking operational turnaround opportunities.

Private equity involvement often focuses on:

- Cost restructuring

- Fleet optimization

- Market exits from unprofitable cities

- Repositioning toward enterprise or subscription models

This reflects industry maturation rather than decline.

As shared mobility integrates deeper into urban infrastructure, long-term capital providers, including infrastructure funds and sustainability-focused investors, may play a larger role in shaping the next phase of industry evolution.

Recent Innovations and Product Developments in Shared Mobility

Innovation Has Shifted Toward Operational Efficiency

Shared mobility innovation is now focused less on rapid expansion and more on improving efficiency, profitability, and regulatory alignment. Platforms are prioritizing optimization over disruption.

Core innovation areas include:

- AI-driven demand forecasting and route optimization

- Dynamic pricing refinement

- Predictive fleet maintenance systems

- Fraud and safety analytics

These improvements directly enhance unit economics and reliability.

Regulatory and City-Focused Tools

To strengthen public-private collaboration, platforms are introducing:

- Data dashboards for municipalities

- Geofencing for controlled device parking

- Emissions tracking and reporting features

These features improve compliance and long-term market stability.

Comparative Innovation Focus by Segment

| Segment | Current Innovation Priority | Strategic Objective |

|---|---|---|

| Ride-hailing | AI routing and EV transition | Margin optimization |

| Car sharing | Fleet electrification and utilization analytics | Asset efficiency |

| Micromobility | Hardware durability and geofencing | Regulatory compliance |

Innovation priorities reflect each segment’s core economic constraints.

Innovation Is Becoming Operational Rather Than Disruptive

The current wave of shared mobility innovation is evolutionary rather than revolutionary. The focus has shifted from market disruption to operational excellence.

Platforms that succeed in this phase will likely be those that:

- Improve lifetime fleet economics

- Integrate electrification seamlessly

- Build regulatory-aligned product features

- Enhance cross-service engagement

As the industry matures, incremental innovation in efficiency, safety, and integration may generate more long-term value than headline-grabbing geographic expansion.

Key Challenges and Structural Risks Facing Shared Mobility Companies

Profitability Remains Uneven

Despite scale, consistent profitability is still a challenge across segments. Cost pressures persist in the form of:

- Driver incentives and retention costs

- Fleet depreciation and maintenance

- Insurance and regulatory compliance expenses

- Technology infrastructure overhead

Margin expansion depends heavily on utilization efficiency and disciplined pricing.

Regulatory and Legal Exposure

Regulation remains one of the most significant structural risks. Changes in labor laws, fleet caps, or pricing rules can materially affect business economics.

Key exposure areas include:

- Driver classification requirements

- Licensing and fleet limitations

- Data privacy and reporting mandates

- Electrification compliance targets

Regulatory divergence across regions adds operational complexity.

Capital Intensity and Asset Risk

Car sharing and micromobility require significant fleet investment, while electrification increases upfront capital needs. Underutilization or hardware failure can quickly erode returns.

Ride-hailing, though more asset-light, faces labor-related cost volatility.

Competitive and Market Saturation Risk

In mature markets, growth has slowed and competition remains intense. Users frequently multi-home across apps, increasing pricing pressure and reducing loyalty.

As the industry matures, risk management and operational resilience are as important as growth. Platforms that balance regulatory alignment, capital discipline, and cost efficiency will be better positioned to sustain long-term expansion.

Strategic Opportunities and Implications for Founders, Operators, and Investors

The Next Phase of Shared Mobility Rewards Precision and Discipline

Shared mobility has entered a structural maturity phase. Large-scale geographic expansion is no longer the primary source of advantage. Instead, opportunity now lies in targeted market whitespace, operational excellence, and ecosystem integration.

For founders, operators, and investors alike, success depends on identifying underserved niches while aligning with regulatory, capital, and sustainability realities.

Where the Real Whitespace Still Exists

Although leading platforms dominate major metropolitan markets, several opportunity zones remain underdeveloped.

High-potential areas include:

- Tier-two cities and peri-urban corridors with limited competition

- Vertical-specific mobility such as healthcare, campus, and industrial transport

- Enterprise-focused mobility programs with contractual demand stability

- Fleet electrification infrastructure and charging hubs

- Data and analytics platforms for urban planning and ESG reporting

These segments often require less direct competition with global incumbents and can offer clearer paths to profitability.

What This Means for Founders and New Entrants

The era of broad, capital-intensive market capture is largely over in mature regions. Competing directly with established ride-hailing giants in saturated cities demands significant capital and regulatory resilience.

More viable founder strategies include:

- Building niche or verticalized mobility solutions

- Developing infrastructure layers such as charging or analytics services

- Leveraging asset-light partnership models

- Designing business models with regulatory compliance embedded from day one

Startups that align with sustainability mandates and enterprise demand are better positioned for defensible growth.

Strategic Priorities for Platform Operators

For existing shared mobility operators, the opportunity is less about new territory and more about extracting value from existing ecosystems.

Core strategic priorities include:

- Improving unit economics through AI-driven optimization

- Accelerating electrification to secure regulatory support

- Expanding subscription and enterprise revenue streams

- Deepening integration with public transport and smart city systems

Operational excellence and capital discipline are now stronger competitive levers than raw expansion speed.

Investor Lens: Risk-Adjusted Opportunity

Investors must evaluate both whitespace opportunities and execution capability. Growth potential alone is insufficient without sustainable economics.

Critical evaluation metrics now include:

- Contribution margin trajectory

- Regulatory exposure across markets

- Capital intensity and fleet risk

- Enterprise revenue diversification

- Electrification readiness

Opportunities with lower capital requirements and stronger policy alignment may deliver superior risk-adjusted returns.

Structural Advantage Is Replacing First-Mover Advantage

The next decade of shared mobility will be shaped by structural capabilities rather than rapid expansion. Durable advantage increasingly depends on:

- Data scale and AI sophistication

- Regulatory credibility and compliance infrastructure

- Electrified fleet strategy

- Enterprise contract depth

- Capital efficiency

Companies that combine focused opportunity capture with disciplined execution will define the industry’s next leadership cohort.

Conclusion and Key Takeaway

The global expansion of shared mobility is no longer defined by experimentation or hyper-growth alone. It is entering a phase of structural integration into urban transport systems. Ride-hailing, car sharing, and micromobility are increasingly embedded within city planning, sustainability mandates, enterprise mobility strategies, and digital ecosystems.

The defining shift is this: shared mobility is evolving from a consumer convenience product into a regulated, capital-intensive, technology-driven infrastructure layer.

Three structural realities stand out:

- Growth is becoming regionally differentiated rather than universally explosive

- Profitability and capital discipline now outweigh raw user expansion

- Electrification and regulatory alignment are becoming non-negotiable

Market leaders are no longer those who expand fastest, but those who execute most efficiently within regulatory and capital constraints.

For decision-makers, the most important insight is that shared mobility is not a short-term trend tied to venture capital cycles. It is anchored in long-term forces:

- Urbanization and congestion pressure

- Rising total cost of private vehicle ownership

- Sustainability regulation and decarbonization mandates

- Digital platform penetration and behavioral shifts toward access

As these forces intensify, shared mobility will likely deepen its integration with energy systems, public transport networks, enterprise travel, and data-driven urban governance.

In practical terms:

- Founders must focus on targeted niches and structural advantages

- Operators must prioritize unit economics, electrification, and ecosystem integration

- Investors must evaluate risk-adjusted scalability, not just revenue growth

Shared mobility’s next decade will reward precision, operational resilience, and regulatory credibility.

The global expansion story continues, but the rules have changed.